Talk:Money supply

| This is the talk page for discussing improvements to the Money supply article. This is not a forum for general discussion of the article's subject. |

Article policies

|

| Find sources: Google (books · news · scholar · free images · WP refs) · FENS · JSTOR · TWL |

| This article is rated C-class on Wikipedia's content assessment scale. It is of interest to the following WikiProjects: | |||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||

American M3[edit]

The American M3 chart should be put back on this page. Autopilot removed it when they put in the Fed's 2010 data.

The M3 is arguably the best measure of the money supply, and simply the fact that the Fed alone has stopped measuring it does not mean that it should not be discussed or visualized in an academic setting.

Is Mandy dumb?[edit]

Mandy deposits $810 that she have borrowed. Interest on credit are higher than those on deposits so why would she do that? —Preceding unsigned comment added by 161.53.242.83 (talk) 10:30, 10 February 2010 (UTC)

- The text seems unfortunate... it is more complicated, e.g. Mandy pays her employees with the money in the hope that their work will return a profit in excess of the interest, and her employees deposit the money. MMMMM742 (talk) 07:45, 11 February 2010 (UTC)

- It is not necessarily that complicated. Mandy e.g. purchases an used car from her friend, who, in turn, deposits the money received from Mandy (which she has borrowed from the bank). Penartur (talk) 18:30, 1 December 2011 (UTC)

Monetary policy by the government[edit]

In the second paragrah it is stated that, "Since most modern economic systems are regulated by governments through monetary policy, ...". In the most of the major economies (such as the US, UK, Euro-area, Australia etc.) the central banks have been made independent of the government, such that they can decide on the best monetary policy without political considerations. Previously this was not the case and monetary policy was in fact decided by the governments, which is still the case in some countries - however this can hardly be considered 'modern' and is not what happens in 'most modern economic systems'. —Preceding unsigned comment added by 124.168.1.154 (talk) 11:46, 20 August 2009 (UTC)

M3[edit]

Does anybody know of or can provide a cited example of M3 for this article?

--Sage Veritas (talk) 20:07, 1 March 2009 (UTC)

Aldur42 (talk) 01:49, 2 March 2010 (UTC) Why are there two marginally reputable commercial websites listed as sources for M3? (Shadow Government Statistics, Now and the Future) We should tell people there are sites that estimate this, and leave it on their own unless a better source can be found.

ANYONE who estimates M3 is inherently "marginally reputable." Just forget about M3 and leave it out of this article. This is in everyone's best interest. — Preceding unsigned comment added by 208.90.11.207 (talk) 04:59, 20 November 2011 (UTC)

Consistency?[edit]

From this article: The rate of interest is the price of money.

From the interest article: "Interest is therefore the price of credit, not the price of money as is commonly - and mistakenly - believed. The percentage of the principal which is paid as fee (the interest), over a certain period of time, is called the interest rate."

Well, which is it? —Preceding unsigned comment added by 68.77.113.94 (talk) 03:35, 9 September 2007 (UTC)

- In the interest article, the word "credit" is being used (not entirely correctly) as a synonym for "borrowed money." Credit is the right to borrow money. For example, when a lender extends you credit, the lender is giving you the right to draw on a fixed sum of money. The extended credit is the "credit limit." You don't pay interest on the credit limit; you only pay interest on the portion that you draw down. The portion that you draw down is money (i.e., M1). Wikiant 13:02, 9 September 2007 (UTC)

- So the interest article should be altered then? It seems pretty insistent that it is correct.68.77.113.94 05:58, 10 September 2007 (UTC)

- Isn't credit the provision of resources rather than the right to borrow resources? The right to borrow resources seems more like credit-worthiness than credit. Moreover credit money is not strictly equivalent to money, and so saying that interest is the price of money seems semantically misleading. It does not even make sense to say that money has a price unless we are referring to the physical price of creating and transferring money. Access to money over time, say earlier than one could normally have access to, seems to have a price, but that is not the 'price of money'.

- This article needs to be more precise and wikipedia needs to be consistent on this issue. 68.77.113.94 00:52, 24 September 2007 (UTC)

- "Credit worthiness" is the borrower's ability to be accepted by lenders as being a "reasonable" risk. Credit worthiness entails no obligation on the part of the lender. "Credit" is an amount of money the lender has agreed to make available to the borrower. There is no such thing as "credit money." If you mean "borrowed money," as far as the definition of money is concerned, the word "borrowed" imparts no distinction. Wikiant 12:07, 24 September 2007 (UTC)

- You are aware that there is an article titled credit money even though you claim that there is no such thing? How many economic articles on wikipedia do you wish to claim are incorrect or should not exist? Do you intend to use standard terminology or not?

- Is any one else going to weigh-on on this? 68.77.113.94 05:42, 25 September 2007 (UTC)

- I would say it is non-standard to use wikipedia as proof a term is standard - that's self-referential. The credit money article has three references, only one of which uses the term credit money. von Mises defines credit money as follows: "A third category may be called credit money, this being that sort of money which constitutes a claim against any physical or legal person." Now, I'm no expert in the terminology of money, but this would seem to be a non-standard definition (me writing an IOU would constitute money under this definition). What he has called credit money seems to be what would simply be called a monetary claim: a claim for money from a person.

- But what is it you're trying to settle? I am not clear what distinction the interest article is trying to make. Interest is the price of borrowing money over time, or the price of money over time. I would say that this is the same as the above, although arguably the statement 'interest is the price of money' is not sufficiently clear. (If one were to be a stickler, money is the price of money: a dollar can be exchanged for one dollar upon presentation.)--Gregalton 13:02, 25 September 2007 (UTC)

- I have no problem with the definition, "interest is the price of borrowing money." Wikiant 13:26, 25 September 2007 (UTC)

A simple example, please, something like this[edit]

What I'm looking for is, right after the list of M0...M3 near the start of the article, something like this, very concrete. Now, what I wrote is probably really wrong, but that's just because of all of the questions that the article doesn't answer properly. They need to be answered, and an example like this is a good way to do it. Note humor and silly phrases illustrating my puzzlement.

M0:

- I have ten us$100 bills. That represents $1000 in the M0 supply for the United States.

- I take one of my $100 bills and burn it in a fire. The US M0 money supply, and my personal net worth, just went down by $100. (?)

M1:

- I take the remaining nine bills and deposit it in my checking account at my bank. The M1 money supply just went up by $900, but since the bank still has the cash, the M0 supply also still has that $900, and they go and lend it out to someone else. (?)

- I write a check for $400, check number 71. The M1 money supply didn't change total, it includes the $400 check and the $500 left in my account.

- I burn check number 71. M1 and my checking account still have $900 because the check is never cashed.

- I write check number 72 for $100 to my friend Alice and she deposits it into her checking account. M1 still has $900 in it, her $100 and my $800.

- I go to lunch with my friend Bianca. She's out of cash, so I lend her $20 and she promises to repay later. Our mutual memory is sortof a virtual check, and the M1 money supply goes up by $20. She repays on Monday. M1 goes down by $20 as we virtually erase the virtual check.

- I get paid a paycheck for $10,000 into my checking account. That chunk of M1 money came from my employer's checking account, which got it from customer payments and stuff. I need it for the rest of these examples.

M2 and higher:

- I write check number 74 for $500 and bring it to the bank and start a Money Market account. Even though the bank is an 'institution', this qualifies as a 'non-institutional money market fund'. Cuz I dunno. M2 goes up by $500 as M1 goes down by $500.

- I write check number 75 for $3000 and invest in Dreyfus Efficiency Restaurants Fund, a mutual fund that invests in small fast-food chains. This $3000 is no longer in M1? In the short term it goes into the company's checking, they go spend it somewhere, and M1 is conserved?. Then they make a ton of money and eventually I cash out and get a check for $6000. This money came from other people's checks when they bought stuff from the company, so it's all in M1? But that means that capital is never created. I don't understand. It's almost like it's in M7 or something, far less liquid than m1 or m2.

- My grandma dies and leaves me her money market fund with $50 million in it. Somehow this is an institutional money market fund... cuz when they started the fund, they checked off this box on their application that says "Do you want your Money Market to be Institutional? [ ] yes [ ] no". So this money is in M3?? You have to have a minimum of what, $5 million, to get it into M3 accounts?

Foreign Currencies:

- I write check number 73 for $200 and bring it to a bank teller and tell him I want to convert it to British Pounds. On this particular day, the exchange rate is exactly 2.00 dollars = 1.00 pound. The bank takes my $200 check, finds some other customer in their branch office in Hong Kong who has pounds and wants dollars, and brokers the trade. (Both bank branch offices have piles of dollars and pounds for just such an occasion.) US M0 still has the $900, although the customer in Hong Kong now has $200 of it. The 100 pound note I walk off with is part of Britain's M0 money supply.

OsamaBinLogin (talk) 05:00, 22 March 2008 (UTC)

- ...which got it from customer payments and stuff... go slow here. There is the other possibility that the employer got it by increasing his overdraft limit. In this case it is "created" money and suddenly M1 increases by that amount (until it is repaid). This is not an unnecessary complication but a vital element of understanding because most "money" is this kind of created money.

Janosabel (talk) 19:51, 9 November 2008 (UTC)

I changed the example to "Laura" instead of me, did some other editing, took out areas I wasn't confident in, and it's now live. It's been there for a year and just one comment.

Thanks, Janosabel. That does get into areas where I'm more fuzzy. I guess there's a lot of areas like that:

- Laura buys $1000 of fashionable handbags with her bank debit card. Just like a check, right?

- Laura buys $1000 of fashionable shoes on her Visa credit card. Suddenly there's $1000 where there was none... or was her $8000 credit limit already a part of M2, so she goes and spends it, no changes? as if she was always borrowing $8000 but only getting charged interest for the times when she actually uses it?

- Laura writes a $5000 check and buys:

- * a Colorado State 'municipal bond'.

- * a US Treasury Bond/bill/note. OOPs you need $25k for that.

- * An IBM corp bond (aka commercial paper)

- * stock in IBM Corp

- * shares of her nephew's privately traded paper company, ironically NOT 'commercial paper'

- * a mutual fund (that includes stocks, Colorado & US and corp bonds...)

- * Shares in Bernie Madoff Investments, Inc (was that really a mutual fund? a family of funds like Fidelity or Vanguard?)

- OK so in each of the above examples, does M1 go down by $5000? Does one of the other Ms go up? Seems like most or all of them are not included in M2 or M3.

- Then, Laura sells said bonds/funds/shares for the going price at the time, $6000. And puts it back into her checking account, so M1 goes up $6000 and something else changes.

- Laura and her friends discover the Lenin Bank, which gives easy credit and easy credit cards. They all sign up for credit cards and HELOCs like crazy. What stops the bank from 'creating' this money?

thanks, whoever answers these questions! You can go and hack it right in the article page yourself. I'll be back. OsamaBinLogin (talk) 02:02, 22 March 2009 (UTC)

This example should be removed, as it is factually incorrect. Banks don't lend out 'extra money that they don't have to keep as reserves.' Banks create their own credit money, which is a lower level of money. The mechanism described in this example, depicting the reserve requirement as a multiplying mechanism, has nothing to do with actual bank operations. Note the contradicting sentence in the previous section that states it correctly: it's about capital requirements and not reserve requirements. Reference: prof. Mitchell's Money multiplier and other myths. [1] — Preceding unsigned comment added by 31.147.174.160 (talk) 18:57, 28 December 2012 (UTC)

I believe there is a mistake in the Example section, but i'm not familiar with subject enought to correct it myself. Line 3 in M1 section states: The M1 money supply increases by $810 when the loan is made. M1 money is created. ( MB = $900 M0 = 0, M1 = $1710, M2 = $1710) Loan isn't actually made at this point however M1 is increased. Loan will be made in Line 7 (to Mandy), increasing M1 again and causing same loan to be double-counted in M1. Gundars.kaulins (talk) 17:42, 14 February 2015 (UTC)

A question for the experts[edit]

- The school-book definition of money is all assets (if you will) that don't pay interest. Would that include the M1 bank deposits? Or do they also pay a little bit of interest sometimes?

- The destinction is made to explain why the money supply increase with lowered rates. Because money doesn't burn so much in the pocket people are more willing to hold then in an interest-free form.

- This is the thought process for that (here a rate HIKE):

- The Fed decides to pay better interest on their loans from banks (the repo lending)

- That makes banks lend more of THEIR assets to the Fed (not the customers money in M1 bank accounts).

- (Note that the rates on the Fed lending affects ALL loans instantly. So it's not just the new loans that pay more, it's all loans.)

- I RETURN the banks can now afford to pay their deposit customers better interest rates.

- That makes people want to move money from their interest-free accounts to interest paying accounts.

- Voilá: The money supply has DECREASED

- If people just moved money from interest-free M1 accounts to interest-bearing M2 accounts (for examplea Money Market Fund that IS included in M2) that would leave the M2 money supply UNCHANGED by this.

- My answer to my own question would be that the rate in the M2 accounts are also made less interesting in relation to other longer term rate investments. For example something just outside the Ms, like a BOND FUND or something like that. And in that way M2 decrease to.

- Anybody have any ideas?--Jerryseinfeld 08:16, 19 July 2006 (UTC)

- I never heard the definition that money doesn't pay interest. I have heard interest described as the "price of money" which contradicts that. M1 bank deposits certainly pay interest. Generally money is defined as a means of exchange, a store of wealth, and a measure of value. M1 money has to be immediately available to buy things - I guess maybe savings accounts don't count as they are intended to be used for saving, whereas current accounts are intended for buying things.

- The rate hike - it's much simpler. When the Fed wants to reduce the money supply, it just sells a repo, i.e. it lends a T-bond to a bank. The bank has to give up lots of cash to the Fed in exchange, and this cash "disappears" because the Fed will not spend it. This means there is less money. When the repo unwinds, the money re-enters the system. I think that the effect of this is to drive up overnight rates (since there is less cash, banks charge more to lend it), and drive down longer maturity rates (since there is a larger supply of t-bonds). --Dilaudid 19:21, 5 June 2007 (UTC)

- "Money" as in M1 either doesn't pay interest (e.g., cash) or pays only enough interest to compensate for inflation (e.g., checking). So, in purchasing power terms (which is what matters), M1 doesn't earn positive interest. Savings aren't M1 because you can't buy anything with a savings account. You must first withdraw the money (as cash) or transfer it to a checking account. Wikiant 20:32, 5 June 2007 (UTC)

- Err - you can get checking accounts that pay interest, at least in the UK. The bank of Scotland offers an account that pays 3.67% real return right now ([1], [2]). You can get checking accounts in the US that pay interest too - the only reason checking accounts don't pay much interest (nominal or real) is because they are costly to run. Where does this idea that M1 doesn't pay interest come from? I've tried googling it and I can't come up with anything. I agree wholeheartedly that you can't buy anything with a savings account, which is why it isn't M1. --Dilaudid 20:33, 18 June 2007 (UTC)

- Ah this explains quite a lot of it. Until 1930 checking accounts in the US were not permitted to pay interest: Demand_account#Interest --Dilaudid 20:36, 18 June 2007 (UTC)

- "Money" as in M1 either doesn't pay interest (e.g., cash) or pays only enough interest to compensate for inflation (e.g., checking). So, in purchasing power terms (which is what matters), M1 doesn't earn positive interest. Savings aren't M1 because you can't buy anything with a savings account. You must first withdraw the money (as cash) or transfer it to a checking account. Wikiant 20:32, 5 June 2007 (UTC)

- The school book definition is far to general to be useful. Anything can serve as money under the right circumstances. It is more helpful to start with the notion of national currency (i.e. circulating legal tender) notes and coins, and bank-created money: credit (euphemism for debt). No?

Janosabel (talk) 20:14, 9 November 2008 (UTC)

the balance sheet example[edit]

Can anyone tell me why the example shows the 1 dollar bond purchased by the C bank from B1 not on B1's liabilities?

thanks

- The example is just not clear enough, if not plain wrong.

As someone with absolutely no background in economics, I found this article left me more confused than before! I was lost after the second sentence. Also it only convers "U.S. Money Supply", with all the examples being "Fed this..." and "Fed that..." The article should either clearly label itself as only addressing Money Supply in the U.S., or be more carefully to acknowledge at the start of each paragraph "In the United States, the Fed handles this situation by doing X,Y, and Z..."

Start of J.G.'s comments:

You may be asking a lot if you want to be able to understand the "money supply" and its effects if you have no background in economics. Not understanding is nothing to be ashamed of, of course! I suggest you consult additional sources, keep reading, and in time you'll return to this article and see that it makes a lot more sense.

Regarding "globalizing" the article, it's hard to make the article inclusive of or descripive of every other economy in the world, because most governments or central banks are not so open as the U.S.'s when it comes to stating their economic policies, principles, and actions. Not that the U.S.'s central bank is always crystal clear.

- I'd suggest there are many economies with policy objectives as transparent as the Fed. The UK, New Zealend, Sweden, Canada, Spain, Finland, Australia and others pursue explicit inflation targeting, more precise than commitments Greenspan would give. More specifically, after the UK government made the Bank of England independent in 1997 policy this transparency has improved further. I'm not qualified to write a 'globalising' update to the entry, but I'd say there's a strong argument for doing so if anyone is? Jamestplunkett 16:47, 23 November 2005 (UTC)

As far as the article focusing on the U.S. central bank, this makes sense inasmuch as the U.S. economy remains the most influential in the international economy for the time being, and it's policies are often "copied" by other central banks. In addition, I would think there are few persons with enough expertise to write about the inner workings of more than a single country's central bank. You would need to have a different person from each country, knowledgable about the history and policies of their own country's central bank.

Know, too, that the actions a central banks can be highly influenced by the political environment they operate in. They may have to make economic decisions based on what is good for the party in power, instead of doing what is best for the economy in an absolute sense. So it may be difficult to state clearly that "in situation A, the Fed (or another central bank) does B, which causes C".

A related thought: the economic situation confronted by a given central bank at a given time may be unique. The combination of factors may be such as was not ever encountered by another central bank before. So the actions of a central bank in those conditions may be unique to those circumstances. Certainly there are basic principles of operation, but they can and have to be shaded and molded to meet the specific situation. This can also make it more difficult to understand central bank policies.

It may help to realize that banking and economics at this level - the level of national goverments and international bodies - is a rather rarified field. It's not supposed to be easily understood by the lay person, any more than nuclear physics or other areas of specialization. But I exaggerate, it's not such a difficult subject. Keep studying; there are many good resources on the Net.

End of J.G.'s comments. 12:45, 18 November 2005 (UTC)

Hard to know where to draw the line on this topic. Basically it's controlling inflation to the right, and measuring well-being to the left, and never the twain shall meet, as it's a zero-sum game. To some on the left, even inflation has a legitimate purpose, in diluting the value of the money held by idle capitalists, which they earned by exploiting loopholes in prior systems of rules...

- Hard to fault the way the article handles it now - the major views (GDP is evil, GDP is the only way to actually measure activity people are willing to pay for and has good correlation to employment, currency integration and simultaneous policy to alleviate the race to the bottom) are all there, basically, although they need me depth and links. Your point about the legit purpose of inflation should be in there, too. Before Milton Friedman it was commonly acknowledged on the right too.

- Inflation has a disproportionate effect on the poor. The idle capitalists simply move their money into assets which hold value, for example index linked bonds or commodities. The poor and older people on fixed annuities don't generally have this option. --dilaudid on 165.222.186.194 14:49, 9 March 2007 (UTC)

" and since GDP can grow for many reasons including manmade disasters and crises, is not correlated with any known means of measuring well-being." this looks like original research, and appears to be incorrect too. Just because something has the occasionaly negative correlation does not mean it is not positively correlated. It seems highly likely GDP is correlated with various measures of well being - now let me find some... "This argument must be balanced against what is nearly dogma among economists". Nearly dogma isn't a concept I've seen before in an encyclopedia. Aren't economists an authority on money supply? --dilaudid on 165.222.186.194 14:49, 9 March 2007 (UTC) This is an article about the money supply anyway, not monetary policy (which is changing the money supply). Why are we worrying about monetary policy in this article? --Dilaudid 10:29, 10 March 2007 (UTC)

Changing measuring GDP To measuring well-being is like changing the weight calculation of a person from the actual force of gravity upon them to an aggregate including their compassion and contribution to the community. So instead of weighing 200lbs, I weigh 170 social weight units because I have participated in volunteer programs and given to the United Way. Therefore, you are not allowed to view me as fat or even suggest that I may suffer heart disease or go over the weight limit for your small private plane. The point I'm trying to make here is that GDP and money supply are simply measures of economic activity not measures of ethical values. There are other indexes like the Human Development Index that are subjective measures of social progress that already exist. Trying to replace GDP is merely confusing the issue by applying a dialectic process to try and resolve an uncomfortable dualism such as Social progress vs. economic progress.

What about M4? [3]

This is also called "Broad money" and I think is unique to the UK.

although I agree with the point on GDP I also think it is unrelated in a money supply post. I d like to see some graph showing the decline in the cash part of money supply and the growth in debt based money. If it could be traced back to early 20th century it would be great as we could see cycles.

GDP[edit]

The problem with GDP is not that it is measured; it is that economists tend to view increasing GDP as "good" and decreasing GDP as "bad" regardless of what that GDP change represents. Thus economists tend to favor anything that increases GDP without looking at the micro effects. (This was one of the arguements in favor of slavery -- that having a large unpaid workforce increased general prosperity.) Jaysbro 15:25, 4 November 2005 (UTC)

- No, having a large unpaid workforce actually decreases current measured GDP, because if they were paid, then their wages and expenses would count towards GDP. It's just a measurement, and most of the time, increase in GDP is good. Of course it's not absolute, but when talking about a robust economy such as the United States, noticeable GDP increases are mostly always good. Of course there might be winners or losers to economic changes (globalization comes to mind, but that can easily remedied by reallocation or policy changes) Leigao84 19:30, 10 May 2007 (UTC)

L[edit]

Can you say where you got this "least liquid" L variable from? The Fed, for one, doesn't seem to measure it. What is the difference between L and M3? --Afelton 20:17, 9 November 2005 (UTC)

GDP[edit]

"although I agree with the point on GDP I also think it is unrelated in a money supply post"

Actually, it is totally related because if the goal of central bankers is to maintain price stability, then that translates into the goal of keeping the money supply rising or falling in step with the rising or falling aggregate supplies of goods and services in the economy in question. Therefore, without the GDP half of the equation, the central bank's whole project of controlling the money supply wouldn't make much sense. Sure, you can talk about money supply as a simple noun without mentioning GDP, but the interesting stuff comes with talking about why money supply is important, and this has everything to do with GDP.

-Robert Nelson

A Good Review of the Moneterists' Understanding[edit]

- This debate needs to be moved to Monetarism. It's not about money supply. --Dilaudid 10:35, 10 March 2007 (UTC)

The discussion of the money supply was easily followed by me, though I am not an economist. However, I took economics in college and have followed the public discussion of monetary policy through the years. My only issue with this article is that it presents one side of the issue: it completely describes a moneterist's understanding, and does not even mention the competing (and major) economic school of keynesianism. It ignores the teachings of John Maynard Keynes on how the money supply should be defined and how they believe it behaves. So what we end up with is a good summary of Milton Friedman's pholosophy, and none of the opposing philosophy of Keynes, which many of us still consider the better policy basis of the two.

[[Reply: Keynesianism is crap. It is responsible for the devaluation of 90%+ of the dollar's worth since 1913 and has led the international financial system into the precarious state it's in now. But if you insist on a Keynesian view as well as a Monetarist view, then you'll have to include the Austrian School view as well.]]

Reply to reply from a non-economist: Your comment seems to be criticizing the entirety of the development of the world's economy since 1913. I am. The past hundred years seem to be enormously more successful economically than any other period in history. Two world wars and the greatest economic depression the world has seen - well, you certainly have raised the bar for us all, haven't you? Perhaps you could clarify your comment?

As for "Keynesianism is crap", I am pretty sure it is not the worst thing to have happened to economic thought during the 20th century. You're right. Socialism and communism. To say the least, it saved lives. These are the lives of the people who had nothing to eat during USA's Great Depression. Who do you think caused it? The Fed. Oh, and by the way Keynesianism became important after the Great Depression, which incidently took place in the 1930s (a while after 1913). And lastly, there are few things better for an economy than its currency's loss of value. Have you lost your mind??? Where do you live? Zimbabwe? I'm sure the loss of the value of the currency was a great thing for the citizens of Weimar Germany in 1923 as they wheeled it around in handcarts in search of a loaf of bread to exchange it for. Because in such a case foreigners are more willing to buy this country's products and so so this country becomes richer in terms of having what to eat, drive, sleep in, etc. So long as the creditor country - China - is willing to keep lending the money. --Cryout 03:00, 8 August 2006 (UTC) Better stick to your knitting.

Would the whiny monetarist please engage in serious debate? Keynesianism is not crap; monetarism is all-but-abandoned among serious Anglophone economists (I don't know what the situation is in Austria :P), and among the active schools of thought on the subject, the two primary contenders are Keynesianism simpliciter and neo-Keynesianism. This isn't the place to debate economic policy, but suffice to say that your views on inflation (oh, sorry, "devaluation") and economic growth are precious. To blame the Great Depression on Keynes, as you seem to do in the previous paragraph, reveals a profound misunderstanding of economic history. The belief that the devaluation of the dollar itself, rather than the negative effects of hyperinflation/inflationary spirals, is a bad thing is textbook idiocy. If you have anything intelligent to say, feel free to say it. 140.247.154.154 04:29, 5 February 2007 (UTC)

Agree with the spirit of this last comment - this isn't a good article and should be rewritten by someone who fully understands the issues. However, monetarism and Keynesianism have much in common - its a mistake to play them off against each other. Keynes knew that monetary policy could be used to stimulate demand, but he emphasised fiscal policy because interest rates were already very low in his day, and he thought printing more money would be inneffectual under those circumstances.

Friedman emphasised the monetary side but thought it best not to intervene lest we make things worse - he advocated steady, measured growth in the monetary aggregates. Today, I would say that, yes, macroeconimists operate in a broadly Keynesian framework in so far as they believe that an overall shortfall of demand causes recessions, and that recessions can be cured by active intervention using a mix of monetary and fiscal policy. But I would add that Friedman filled in the detail of much of this framework, dramatically improving our understanding of monetary and fiscal policy and their limitations (his work on the natural rate of unemployment and permanent income theory fully establish him as a brilliant economist who has had a lasting impact). The basic thrust of this article should be as follows:

1. Recessions are caused by a shortfall of aggregate demand relative to the potential output of the economy (not everything than can be produced can be sold because of lack of demand, so some resources will end up unemployed). 2. The good news is that monetary policy can be used to control demand. Print money and you increase demand, take money out of circulation and you reduce demand. 3. The basic rule is: if the economy is in recession, print money at a greater rate until demand is equal with potential supply, then ease off! If you print too much money then demand will exceed supply and, rather than stimulating more production, you will just get inflation. 4. Once this basic logic of monetary policy is stated, then the more detailed M1, M2 stuff can be explored. 5. Ditch the stuff on alternative GDP measures - it is hopelessly confused!Pjtobe 09:39, 19 February 2007 (UTC)

Innaccuracy[edit]

[Deleted] -- did not realize there was that much cash out there 68.196.112.152 16:38, 11 August 2006 (UTC)Karl

What are IRA and Keogh balances?[edit]

What are IRA and Keogh balances?--Samnikal 13:23, 19 November 2006 (UTC)

Arguments and Criticism[edit]

I am going to delete the last sentence of this since it is highly, highly debatable...

"In the last 10 to 15 years, there is good evidence that many modern central banks have become relatively adept at manipulation of the money supply, leading to a smoother business cycle, with recessions tending to be smaller and less frequent than in earlier decades.

- That's what sent me scurrying to the talk page. If the Fed had not changed the way the CPI is calculated, and eliminated the M3, and if the definition of the federal deficit had not changed, would the "cycle" look smooth? or would it look terrifying? It is very un-Wikipedia to say there is "good evidence" without supplying a shred of it. Jive Dadson 20:18, 20 July 2007 (UTC)

I don't think the 17 year recession (unless you want to call it something else) in Japan, or the recessions of the early 1990's and early 2000's are regarded as smaller, since they were two of the deepest recessions on modern record and corresponded to traditional timeframes for a recession... The only verifiable aspect of economics in the last 10-15 years in the United States would be the extent to which economic forecasting has statistically fallen out of touch with reality... This sentence's phrase either needs to be revised to reflect a "safe" statement about reality or be deleted... Stevenmitchell 19:47, 4 April 2007 (UTC)

No, the statement is accurate on average. Japan is the exception and even there the volatility of output has been low (as has been the growth rate). Both the 1990's recession and the 2000 recession have been the shortest and mildest on record (pretty much). I'm gonna add a reference to the sentence. Having said that the paragraph could be written in better style. radek 00:06, 18 April 2007 (UTC)

Also the Japanese recession is not due to monetary policy but reflects a deeper problem with their financial sector. Leigao84 19:34, 10 May 2007 (UTC)

Anyone else think this statement is plainly wrong:

"By taking money out of circulation, the central bank can reduce demand. "

Isn't the other way around?Leigao84 06:56, 18 May 2007 (UTC)

Less money (more bonds) in circulation means higher interest rates (lower bond prices) which in the standard framework means a reduction in aggregate demand. I think it's basically right.radek 16:54, 18 May 2007 (UTC)

- The problem is that there is no adjective attached to "demand." Taking money out of circulation reduces the supply of money. This, in turn causes interest rates to rise. The rise in interest rates reduces aggregate demand. Wikiant 19:08, 18 May 2007 (UTC)

- Strictly speaking that only works for central banks not operating under a fixed or pegged exchange rate regime. In general central banks do not conduct monetary policy this way. Whilst theoretically true the article should not give the reader the impression that this is a common way for central banks to conduct policy. Last but not least it rests on the idea that prices are sticky since in general prices will adjust leaving no real effects. The idea of central banks "sucking" liquidity by issuing bonds is nothing new, it just isn't a primary tool and in many cases not on the agenda since it affects interest rates. Perhaps this is better understood by remembering that the idea that central banks can increase demand by increasing the money supply has generally been abandonded. MartinDK 17:27, 14 July 2007 (UTC)

- Question from fifteen years later

How does the recession of 2008 play into these arguments? Anyone?Dstar3k (talk) 21:47, 27 November 2022 (UTC)

Money demand leads here?[edit]

Hmm, this article talks about money supply and very little on money supply. So, why money demand is redirected here? __earth (Talk) 07:18, 1 July 2007 (UTC)

I also think money demand deserves its own page 116.240.210.194 (talk) 12/9/08. —Preceding undated comment was added at 17:26, 11 September 2008 (UTC).

Funny Munny Supply[edit]

If I may draw one's attention to the law and constitution for the U.S.A., only gold and silver coin are money (denominated as dollars).

From the United States Code:

"The terms lawful money and lawful money of the United States shall be construed to mean gold or silver coin of the United States..."

Title 12 USC Sec. 152.

In fact, Federal Reserve Notes are obligations to PAY dollars (silver or gold) pursuant to Title 12 USC Sec. 411. But since 1933, the government won't redeem their notes with dollars. Ergo, Federal Reserve notes have no par value (legalese for worthless).

So what makes repudiated notes into "legal tender"?

The one owed a debt must accept his own note, as tender. In other words, if YOU issue an I.O.U., you must accept it as tender if it comes back to you. It makes sense that Federal Reserve notes are accepted by the government as tender in payment of taxes and fees owed to them. It's their note. Only people who are obligated to pay on an I.O.U. are obligated to accept worthless paper as legal tender.

"Federal reserve notes are legal tender in absence of objection thereto." MacLeod v. Hoover (1925) 159 La 244, 105 So. 305

What changed so that all people could no longer object to the tender of worthless notes?

What made every American into a debtor obligated to pay the national debt?

How does new paper money (new debt instruments) get authorized to be printed?

When does the interest get created?

How can constitutional government officers ignore the constitution?

They don't...

According to Title 31 of the U.S. code:

31 USC Sec. 5112. Denominations, specifications, and design of coins

(e)(1) ...weight 31.103 grams;

(e)(4) have inscriptions ... 1 Oz. Fine Silver ... One Dollar.

So the government still knows that a one ounce silver coin is a dollar. But how many people have actually used dollars? I suspect that no one, since 1933, has ever used real dollars to pay their debts. Frankly, it costs many more Federal Reserve notes (dollar bills) to buy one real dollar coin. No one would be foolish to pay a debt with good money, when bad money will do the job.

THE BIG QUESTION

How can debt (notes) pay off the national debt (8.89 trillion dollars as of 7/20/2007)?

ANSWER

It can't.

So the national debt is a legal obligation to pay gold or silver dollars.

8.89 trillion equates to the obligation to pay 6,667,500,000,000 troy ounces of silver, or 444,500,000,000 troy ounces of gold. And based on current mining rates, it would only take 800,000 years to mine the bullion to pay off the national debt with lawful money - if the interest was frozen right now.

Perhaps, academia would not wish us to ask them to account for the discrepancy in their Economics "science". It's obvious no politician nor public official would like to answer these questions. Too many unpleasant words come to mind, when one thinks of these things.

Jetgraphics 19:07, 20 July 2007 (UTC)

- If you don't intend to comment on the article, this is spam - Crosbiesmith 19:53, 20 July 2007 (UTC)

No it is not spam, it is the situation just before 1980 when the Hunt brothers, blew the silver market to the sky and en masse people went to the treasury to collect silver for their dollars. In that event the treasuty dicided to abandon the priciple of silver backed USD. —Preceding unsigned comment added by 87.211.128.236 (talk) 22:40, 3 September 2007 (UTC)

- I have no idea what the design of the Silver Dollar which is no longer in mass circulation have anything to do with debt. Look just under section E and you find Section F.

- (f) Silver Coins.—

- (1) Sale price.— The Secretary shall sell the coins minted under subsection (e) to the public at a price equal to the market value of the bullion at the time of sale, plus the cost of minting, marketing, and distributing such coins (including labor, materials, dies, use of machinery, and promotional and overhead expenses).

- So the government can sell these 1 dollar coins at the current market price of silver. Of course no one will want it unless for collections purposes. This does not mean that one dollar is based on silver, it just says that the government have have to make enough of these silver dollar coins.

- And please, paper money is not debt. US Government debt is printed on outstanding US Government Bond Notes. The government can really make money out of thin air! It's the power of seigniorage. The reason they don't is because it will cause hyper inflation and destabilize the economy. Leigao84 (talk) 21:45, 15 February 2008 (UTC)

Quote: "The government can really make money out of thin air! It's the power of seigniorage. The reason they don't is because it will cause hyper inflation and destabilize the economy."

Too late. Thankyou, come again to the Federal Reserve Bank. We now accept Euro's and Amero's. —Preceding unsigned comment added by 94.192.246.138 (talk) 13:43, 4 January 2009 (UTC)

According to the Constitution, Article 1, Section 8 "The Congress shall have Power ... To coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures", and Section 10 "No State shall enter into any Treaty, Alliance, or Confederation; grant Letters of Marque and Reprisal; coin Money; emit Bills of Credit; make any Thing but gold and silver Coin a Tender in Payment of Debts" so it seems like Congress has the power, the states don't. MMMMM742 (talk) 00:00, 17 January 2010 (UTC)

Note: "to COIN MONEY" means to stamp bullion. Government cannot create bullion, ergo, it cannot create money. Neither can banks. Jetgraphics (talk) 15:52, 15 July 2020 (UTC)

Monetary exchange equation[edit]

Would it not be correct to classify this as a theory of Keynesian economics? - MSTCrow 22:36, 7 August 2007 (UTC)

- It would be incorrect to classify the money supply equation as a theory of Keynesian economics because it is based on the Quanity Theory of Money (a 17th century theory); though, the velocity of money is an addition from Friedman(20th century) and Fisher(19th century) and may have some basis within Keynesian thought. This equation is also used by classical economist and Monetarists and this section could be expanded to explain how the different economic schools of thought use this equation.--EGeek 19:18, 10 August 2007 (UTC)

- It needs to be more clearly written that it is a simple and additional tool at measuring inflation. It is incapable of measuring the real value of anything as it disregards the subjective portion of trade. Both this section and the actual Equation of exchange Page are poorly written and do not really educate of it's purpose other then the existence of another algebraic formula. Also this formula from who's theory's it was derived in recent and historical times is highly disputed quiet remarkely easily considered flawed as mentioned by MSTCrow above. That however is a whole other debate and not really relevant to this article. A whole other page could be created to the different types of Theory's of Value. Beaon (talk) 00:23, 7 January 2009 (UTC)

Money supply is important because it is linked to inflation by the "monetary exchange equation":

- Also, This statement needs to be re-written. It makes it appear that Money Supply is linked to inflation which is wrong. Money supply in itself is dumb and cannot expand or contract on its own. Money supply is only a representation of inflation. Inflation itself is linked to monetary policy, usually in regards to the manipulation of the commodity known as credit. Beaon (talk) 00:23, 7 January 2009 (UTC)

As one who had studied this equation in school and believed it for some years, I have some considerations for those others who, like me, see the simplicity and obvious correctness of it. First, the equation does not take into account of the fact that price inflation begins in the geographical location of the insertion point of the new currency. That is, in the location where the government spent the initial funds, prices rise due to the new volume and some additional velocity of circulation. At that point, it radiates out into the general economy like ripples in a pond. The conclusion is obvious: prices do not rise equally through the economy all at once but in waves as the new money is spent or invested. Secondly, the new rise in prices and earnings cause individuals and companies to reassess their need to hold cash reserves and where to spend their newly received funding. Their marginal utilities change in real time depending on this re-assessment and demand and supply schedules are revised. This will also affect the price level and may actually cause prices to decline rather than rise. Usually however, velocity will increase for various reasons, including the "Hot Potato" effect, and a possible reduced need for cash reserves by industry. Anticipation of future trends will affect the velocity of exchange just as much as the quantity of money in circulation. All that being said, it is not even possible to measure Q, M, or V anyway, and barely possible to measure P. D.Lingerfelt 6/16/08

Merge M4 money supply into this article[edit]

Any objections? Sonic Craze 00:36, 24 October 2007 (UTC)

- None here. I think this merger is a good idea. -FrankTobia (talk) 18:38, 17 December 2007 (UTC)

- No, I agree it's a great idea. MilesAgain (talk) 19:14, 21 December 2007 (UTC)

- Agree. It makes sense. --Gherrington (talk) 22:02, 1 January 2008 (UTC)

- There is also a separate page on monetary base. Finnancier (talk) 04:19, 2 February 2008 (UTC)

- Support. Monetary base should be merged/removed also Ummonk (talk) 19:12, 7 November 2008 (UTC)

- There is also a separate page on monetary base. Finnancier (talk) 04:19, 2 February 2008 (UTC)

- Support Merge Morphh (talk) 3:34, 24 February 2008 (UTC)

Graphic chart format[edit]

Can the two graphic charts in this article ("Components of US money supply (M1, M2, and M3) since 1959" AND "US M3 money supply as a proportion of gross domestic product") be modified? It appears that a background texture or fill pattern is causing the charts to print a black background that obscures some of the data or titles.

Chart scales[edit]

All the charts need converting to log scales on their y axes to be useful visual representations of the underlying data. —Preceding unsigned comment added by 87.194.2.217 (talk) 21:16, 16 April 2008 (UTC)

Recent Money Supply changes[edit]

I have removed the "Recent Money Supply changes" section. I would consider this unencyclopedic; it would need to be constantly updated otherwise it would be outdated and therefore not useful. Gary King (talk) 21:57, 19 February 2008 (UTC)

- Can you instead provide a reference link to a site which provides the M3 "estimate" ? These numbers aren't real but most people who visit this page looking for "money supply" are probably looking for what that number is. You don't currently provide a link to this data anywhere. I would say its important for the article. —Preceding unsigned comment added by Mozkill (talk • contribs) 19:46, 24 June 2008 (UTC)

Definition of Inflation[edit]

In the Purpose section of the article it states: "The money supply is considered an important instrument for controlling inflation by economists who say that growth in money supply will only lead to inflation if money demand is stable." However, according to historical definition, inflation IS by definition an increase in the money supply (ie. inflation is a cause [increase in money supply], not an effect [prices of things increase]). Can we fit this in here somehow while maintaining NPOV? 98.223.131.191 (talk) 07:30, 8 July 2008 (UTC)

- This is incorrect. The defintion of inflation is a positive change in a price index. To say that "inflation is a cause of an increase in the money supply" makes no sense. Inflation is endogenous while the money supply is exogenous. Wikiant (talk) 13:57, 8 July 2008 (UTC)

- Actually, monetarism is based on the Quantity theory of money which directly relates the quanity of money (supply) with economic output (demand). Not all economists agree on this, the statement should read "...inflation by monetarists, who say..." instead. Also the consumer price index only a measures one type of inflation. The GDP deflator is the measure of inflation that absorbs economic output, which does not use the consumer price index. What type of inflation is suppose to be represented in the article? -- EGeek (talk) 04:17, 11 July 2008 (UTC)

Question[edit]

In the second line, is monetary aggregate a methodology to measure money supply or is it a synonym of money supply? Zain Ebrahim (talk) 12:43, 20 July 2008 (UTC)

- Money supply is a vague and general term. Monetary aggregates are those measures of money supply that combine more than one 'type' of money. ie. M2 (savings deposit + checking deposits + physical money (cash)] is a monetary aggregate. lk (talk) 05:08, 18 September 2008 (UTC)

"While the monetarists presume that velocity is relatively stable" - This statement should be sourced. I don't think the Monetarists make this claim at all. For example, see Milton Friedman, one of the principle monetarists, in his "Great Contraction" chapter in the Monetary History of the United States. This chapter about the Great Depression discusses in great depth the changes in the velocity of money as a result of high rates of bank collapses. So without some support for this statement, it creates a straw man argument used to bash monetary theory. —Preceding unsigned comment added by 66.137.224.246 (talk) 16:33, 24 November 2008 (UTC)

I found this more up-to-date chart you might consider using. It illustrates what happens to an economy's money supply as it rolls into a recession/depression.

http://www.shadowstats.com/imgs/sgs-m3.gif?hl=ad —Preceding unsigned comment added by 96.247.199.48 (talk) 19:36, 10 December 2008 (UTC)

{kind=link}

credit money system question[edit]

Imaginary Federal government creates money out of thin air: 200,000

200,000 is deposited into the world bank

Bank loans out 180,000 for a home, which it creates out of thin air

Possible correction here: the only ones creating money is the Fed, the bank loans out 180k, keeping 20k as reserve... It could work both ways, according to: http://en.wikipedia.org/wiki/Fractional-reserve_banking#A_Simple_Example:_A_Single_Bank

Now there is 380,000 existing

Assuming for simplicity that the 180k is redeposited, the bank has 200k plus the home, but they owe the Fed 200K and the depositors 180k

scenario 1:

Mortgage gets paid back

Money in circulation is reduced by 180,000

Bank has 200,000 + interest

Interest came from other loans the bank made

Money supply has to keep increasing in order for people to be able to pay interest

scenario 2:

Mortgage gets defaulted on

There is still 380,000 in circulation...

200,000 in the bank (after all, didn't the money get created out of thin air, to the limit of the required reserves?)

180,000 to the people that got paid for the house

Bank owns the home!

scenario 3:

Mortgage gets defaulted on

There is still 200,000 in circulation...

Bank had 200,000, but according to rules it is supposed to delete 180k

20,000 in the bank

180,000 to the people that got paid for the house

Those people deposit the 180,000 in the bank

Bank owns the home!

Bank still has 200,000, just in different accounts

Bank never had 200k. They just make money on interest. They owe the Fed 200K, They owe the depositors 180K. They have a home and they have the 20K reserves, or they have 200K reserves, depending on which branch of the following example you want to follow: http://en.wikipedia.org/wiki/Fractional-reserve_banking#A_Simple_Example:_A_Single_Bank

People are deleveraging, reducing the money in circulation. In this situation, where are people going to get the money to pay off loans + interest??? With the money supply decreasing as people pay off loans, many can't --Campoftheamericas (talk) 17:07, 31 January 2009 (UTC) I guess scenario 3 is happening. Bank should always have the original reserves, since everyone deposits into the Bank anyway.

People are buying treasury bonds because they feel these are safe. Therefore, cash goes to the central bank, INCREASING the amount of reserves even more.

Consider this:

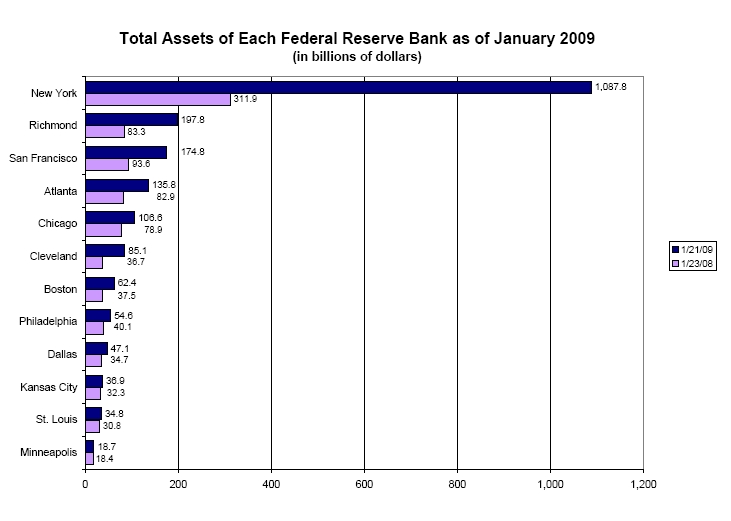

http://upload.wikimedia.org/wikipedia/commons/5/5b/Total_assets_of_each_Federal_Reserve_Bank.jpg

which came from here:

http://en.wikipedia.org/wiki/Federal_Reserve_System#Federal_Reserve_Banks

{kind=link}

Do you think the Fed may have plotted this downturn all along to load up on real assets? Are these real assets (real estate, etc), or some financial junk? So there is a "bad bank" after all! They don't need to make another.

The flogging of all the commercial/private banks today is a good cover up (even if they deserved it).

Please make points against this theory, like, the Fed will eventually sell the assets and give the profits to pay off the U.S. deficit, or something to that effect. If there should be transparency, it should be at the Fed!

The "Simple Example" Part of the explanation[edit]

This is my first time participating in the information side of Wikipedia and I have only done it because I feel that one example maybe incorrect and hope discussion helps confirm/corrects the example. - Laura goes to lunch with her friend Bianca. Bianca's out of cash, so Laura lends her $20 and she promises to repay later. Their mutual memory is a form of virtual check, and the M1 money supply goes up by $20. Bianca repays on Monday. M1 goes down by $20 as the debt is satisfied.

-I could be wrong but here goes, Here is the rub with this idea of personal credit inflating the money supply or M1 in this example. Laura who is the Lender here is not increasing the money supply because there is no fractional reserve lending that is taking place. In the hypo leading up to it Laura has 900$ in an account I believe. Say she lends out 20$ to Bianca, she now has 880$, 20$ N/R, and Bianca has 20$. Is the 20$ N/R chequebook money as is used when a financial intermediary participates in it. If so does this even fit into the definition of M1 money supply as it is stated above the example?

Mvalioll (talk) 05:06, 8 April 2009 (UTC)

- I have removed the example. The definition of M1 money supply does not include the $20 Laura lent Bianca. - Crosbiesmith (talk) 17:37, 8 April 2009 (UTC)

At Least One Footnote Antiquated[edit]

Chicago Fed - Our Central Bank: http://www.chicagofed.org/consumer_information/the_fed_our_central_bank.cfm as of now ref#15. Links doesn't work.

70.18.23.71 (talk) 18:54, 19 April 2009 (UTC)20090419 Footnote 8, currently http://dollardaze.org/blog/?post_id=00565 does not appear to exist.

The Laura example[edit]

I really like that there's a Laura example so the reader can follow along with a sequence of steps to understand. To be more complete, the example should name the borrower that the bank lends $900, and explain what happens when the borrower repays the $900 (or, better, a fraction like $600) to the bank. Tempshill (talk) 21:55, 9 May 2009 (UTC)

"Example", error[edit]

In the "Example-M1", the sentence: "Since the bank still has the deposit on its books, the M0 supply also still has the original $900, as does M1, because M1 includes M0. " is wrong, conflicting with the definition of M0 above (deposits are not part of M0). At this point in the example the amount of M0 depends on what happened to the $810 first loan. If it is deposited into a second bank (but not loaned out yet) then a minimum of $81 is deposited into the central bank (M0 is now $171=$81 + $90). Because it was not loaned out by the 2nd bank the remaining $729 are excess reserves which may or may not be deposited into the central bank. Yes after the original $900 makes it way completely through the web of the banking system with each bank loaning the maximum amount out, the M0 component will go back up to $900 (this $900 will be composed entirely of reserves), but at this stage, with one deposit + one loan the M0 component generally not be $900. Jeffbood (talk) 16:19, 7 July 2009 (UTC)

Example[edit]

I don't think the example is correct in the following steps:

* Laura deposits her paycheck for $5,000 in her checking account. That part of M1 money came from her employer's checking account. No change in total M1 based on the original $ 900. (M0 = $900, M1 = $1710)

M2

* Laura writes check number 7774 for $1000 and brings it to the bank to start a Money Market account. M1 goes down by $1000, but M2 stayed the same, because M2 includes the Money Market account, but also everything in M1. (M0 = $900, M1 = $800, M2 = $1800)

In the first step, M1=1710. In the second step, "M1 goes down by $1000". Doesn't 1710 - 1000 = 710? So that would mean M1 = 710, and M2 = 1710 in the second step. Also, in step 2, "M2 stayed the same". I think 1710 is the same as 1710 not 1800 (M2 includes all of M1).

In step 1, how can M1 be 1710, when there was a checking account with an amount of at least 5000? M1 includes checkable deposits regardless of whose account it was (her employer's or her's). If the example is only from the point of view of Laura's impact on the money supply, then it would be helpful to say so.

Eiflerian (talk) 00:33, 29 July 2009 (UTC)

Incorrect Examples of How Fractional Reserve Lending is used in Your Article.[edit]

The calculations that you have used in this article(Laura) to calculate generated loan credit for the bank as derived from the fractional reserve lending multiple of 1:10 from the depositor's $900 deposit is incorrect.

A Simple Correct Example

The depositor deposits $100 into the bank.

The bank is now allowed to generate, using fractional reserve lending at 1:10, $900 for loans.

The deposited $100 held in the bank as physical cash represents the 10% of the whole -- ie deposit($100) + credit($900). And the $900 is generated out of thin air for the bank's loan assets.

Reference http://www.basicincome.com/basic_banks.htm

- The bank is not allowed to lend more than a fraction of the deposited money. In order to get to the multiplier you mentioned, the loaned money has to flow back into the bank (e.g. the borrower buys a car, the car dealer deposits the money). Then the bank is again allowed to lend a part of this money. If the reserve requirement is 10%, then with the new loan the money supply has increased from $100 to $100 + $90 + $81 = $271. This can go on as a geometric series, converging to a money supply of 10 times the original. MMMMM742 (talk) 11:00, 25 April 2010 (UTC)

Source? Your description seems to oversimplify things, There has to be multiple "redeposits" of the money first before you can arrive at that figure, However, the $100 was also created out of thin air. Hackwrench (talk) 13:30, 12 October 2015 (UTC)

Effects of Changes in the Money Supply[edit]

The article describes money supply at some length and it is quite obviously a complex subject. But where can I find some information on the effects of changes in the money supply? For example, around the beginning of this year (2009), the Fed introduced a step change in the money supply that doubled the U.S M0 or Monetary Base thereby devaluing the Dollar. What is the expected effect of this action? Does anyone know? Do theories exist that economic analysts would use to divine the results of a given action or is it more of a by-guess-and-by-gosh kind of thing?

The article argues between Keynes and Friedman but doesn't provide much insight into the dynamics of the system. As I see it, Dollars in the free market are a commodity like wheat or gold and are subject to laws of supply and demand. The Dollar is worth so much less today than, say, fifty years ago because the market is glutted with them. Increasing the M0 is going to drive down the value of the Dollar. For those buying U.S. goods, this is a windfall because they can get more for their Pounds or Yen or whatever. Going the other way, however, it raises the price of foreign goods to U.S. buyers and is, in effect, a tariff, i.e., protectionist. Is this correct?

It would seem that changes in monetary policy would produce predictable effects. If not here then where should the reader look? --Virgil H. Soule (talk) 19:04, 24 October 2009 (UTC)

- I recommend looking at the history of direct targetting of the money supply, particularly in the 1980s and especially in countries with excellent statistics like the US or UK. The central problems of predicting monetary policy effects with any sort of precision are that (a) the velocity of money is not a constant, (b) monetary policy action x will have an unpredictable effect on the money supply and therefore won't have a clear effect y on the economy as a whole, (c) monetary policy is not isolated from the rest of macroeconomic policy, eg. a change in public borrowing can have an effect on the money supply, which is why Gladstonian "balance-the-budget" thinking, as was popular in the UK in the 1990s and early turn of the century, is a crude but rather effective macroeconomic tool.

On the other hand, one shouldn't take this scepticism too far: if you're looking for the degree that the impact of monetary policy can be understood, check out some modern monetary economists like Tim Congdon. Monetary policy is in roughly the position of cannon-aiming in the 19th century- you can predict which way the cannonball will go and the general area that it will land in, but the kind of precision you find in modern artillery was inconceivable. The same is true for monetary policy and if you can work out a way of accurately predicting the impact of either policy changes on the money supply or the money supply on macroeconomic conditions, your Nobel Prize awaits.Pragmatism24 (talk) 16:07, 5 November 2009 (UTC)

Market value or face value[edit]

In measures of the money supply including money market securities like commercial paper, is it the market value of these securities or the face value/value at maturity (assuming there is no default) that contributes to e.g. an M3 measure? MMMMM742 (talk) 19:55, 13 January 2010 (UTC)

How much of the world GDP is available in printed and coined money ?[edit]

Anybody knows where I can find that? Like in $ bills and $ coins and € bills and € coins, etc. and all that added up? I thought that is what is what the articles on "Money market" or "Money Supply" would be about? Thx. --SvenAERTS (talk) 01:04, 25 January 2010 (UTC) —Preceding unsigned comment added by SvenAERTS (talk • contribs)

- GDP is annual production (a flow measure) while money is a stock measure, so your question doesn't make sense. You may mean to ask, "what is the total value of coins and bills issued by the various central banks?" The "coins and bills" we call M0 (see money supply). Note that that is only a small portion of the money supply -- most of the money supply is not in the form of coins and bills. Wikiant (talk) 13:39, 25 January 2010 (UTC)

- The question does make sense because the answer might tell you something about the velocity of money (e.g. Japan has a lower velocity of money, and a higher ratio of various measures of money supply and GDP than the U.S.). For the data you should look on the websites of the central banks - the Fed's balance sheet can be found here (updated weekly). Currently the currency in circulation (M0) is 918 billion dollars. MMMMM742 (talk) 14:54, 30 January 2010 (UTC)

A few problems[edit]

Error in example + hypothesis about how it happened: In "Example", when going from the end of M1 to the beginning of M2, the numbers don't match. The check numbers went from 7772 to 7774, so I guess some actions in the middle were deleted. In such case, the rest of the example should be re-written. This repeats later, in the beginning of Foreign Exchange, where it says that "US M0 still has the $900", although it was $4900 just before. In this case, bank note numbers jumped from 7774 to 7776.

Also, there's an inconsistency between the example and the table above. In the example, in the beginning of M1, it says that all of the $900 is "part of the bank's excess reserves", so MB = $900, M0 = 0, M1 = $900, M2 = $900. But according to the table, access reserves are only part of MB and not of M1 or M2. —Preceding unsigned comment added by 98.209.17.185 (talk) 03:49, 26 January 2010 (UTC)

M3[edit]

The two sites referenced for M3 calculations, especially the "shadowstats" onel are sites with clear biases and are not credible sources at all. Can anybody tell me why these two references shouldn't be deleted? --Dwarnr (talk) 20:33, 4 February 2010 (UTC)

M0 MB M1 M2 M3 MZM[edit]

The bullets below the "type of money" chart are a tease; they are more like notes, one says what a category is not rather than what it is. Money supply type definitions in a short format should collectively describe what the money supply is.

Major categories:

- MB: total currency

- checking deposits

- etc

- M1: ?? (this is the category most commonly referred to by other pages)

- M2: the amount of money in circulation

- M3: ??

Other:

- MZM: Money with zero maturity, supply of financial assets redeemable at par on demand <- not understandable by the average wiki reader

- M0: monetary base in some countries, or narrow money

--John Bessa (talk) 13:02, 1 August 2010 (UTC)

The M1 money supply increased by $810 when the loan is made. M1 the money has been created. ( MB = $900 M0 = 0, M1 = $1710, M2 = $1710)[edit]

"The M1 money supply increased by $810 when the loan is made. M1 the money has been created. ( MB = $900 M0 = 0, M1 = $1710, M2 = $1710)" M0 should be $810, not $0, because the person taking a loan receives 8 $100 bills and 1 $10 bill. I propose the following change, but please confirm if my understanding of M0 is correct: "The M1 money supply increased by $810 when the loan is made. M1 the money has been created. ( MB = $900 M0 = $810, M1 = $1710, M2 = $1710)"

November 3, 2010 131.107.0.81 (talk) 20:46, 3 November 2010 (UTC)

Japanese money supply graph - surely some mistake![edit]

The graph purporting to show the assorted monetary aggregates for Japan must surely be wrong. The supposed units are "100 yen" which is of the order of one dollar. So the monetary aggregates for Japan look to be on the order of 10million dollars. This can not be right, its far too small - surely there are some missing zeros! Reissgo (talk) 11:56, 14 March 2011 (UTC)

Looking at this: (http://timetric.com/index/LCGyVHjfSCalqfFJFv1H_Q/) would lead me to believe that the numbers on the left hand side of the current Wikipedia graph are in fact billions of Yen - not "100 yen". Reissgo (talk) 15:40, 17 March 2011 (UTC)

All the links to the Bank of Japan site from this article are broken. I've got the following graph from their official site:

File:Bank of Japan money supply graph 1980-2011.png

{kind=link}

Units are 100 millions of Yen, and the blue color denotes "Average amounts outstanding" (M2?), while the red color denotes "banknotes in circulation" (M0?). The graph bears no resemblance to the graph given in Wikipedia article (even under the assumption that wikipedia's graph has the wrong units). Also, wikipedia's graph seems to have its colors messed (e.g. it is written that blue color denotes cash and the red color denotes M1, while there are no such colors on the graph; however, the brown color on the graph is not described anywhere). Penartur (talk) 05:39, 14 November 2011 (UTC)

Arguments[edit]

It is only the US Central Bank (the FED) that has this dual mandate (inflation and unemployment). Other country's central banks target inflation only, e.g. the ECB, which targets 'price stability' i.e. low inflation. This should be explicitly stated to avoid confusing readers. — Preceding unsigned comment added by Pmacaodh (talk • contribs) 10:29, 1 September 2011 (UTC)

Reference Australia[edit]

The link to the RBA website for the Australian money definition doesn't work any more. 202.171.164.59 (talk) 05:05, 11 October 2011 (UTC)

Include link to Divisia Monetary Aggregates ?[edit]

http://en.wikipedia.org/wiki/Divisia_monetary_aggregates_index

Also, perhaps include a couple of sentences about this? Namely, these indices are the same idea but could be better than simple-sum aggregates?

I am adding the suggestion to the "Divisia Monetary Aggregates" page. (Sorry, just joined wiki 5 minutes ago. When I get more comfortable I may come back and do the changes myself...) — Preceding unsigned comment added by Dvorak oneday (talk • contribs) 23:23, 3 January 2012 (UTC)

U.S. Monetary base vs. St.Louis Adjusted Monetary Base : clarification please[edit]

The graph for the U.S. monetary base shown in this article is very different than the graph of the St.Louis adjusted monetary base graph found here. Please explain in the article. — Preceding unsigned comment added by 207.179.172.216 (talk) 19:23, 13 January 2012 (UTC)

.svg){kind=link}

What happens to M2,if Mandy goes bankrupt?[edit]

What happens to M2,if Mandy goes bankrupt? Bank will acknowledge that his $810 loan will never be re-payed. In such case,the sum $810 will be subtracted from M2? — Preceding unsigned comment added by 80.188.193.66 (talk) 08:53, 3 April 2012 (UTC)

- Nothing. The bank will write off the loan and deduct $810 from the asset side of its balance sheet; the monetary aggregates look only at the liability side. Ferridder (talk) 18:13, 18 April 2012 (UTC)

The $810 credit lent to Mandy[edit]

The bank cannot create $810 in credit money without there being a borrower for the money, e.g. Mandy. Same thing with the second time the money is lent out. I suggest to modify the example by not updating M1,M2 until the loan(s) have been made. Comments? Ferridder (talk) 18:13, 18 April 2012 (UTC)

Definitions of Money supply (M1, M2) need a defined purpose.[edit]

I am no expert in $$$ but I find this article poorly written because I see government (/central bank)accountability as most important in the concept of 'money (currency) supply'.

As mentioned, M0 refers to the total amount of printed currency in circulation (owned by persons other than the issuing authority), M1 meaning M0 plus demand deposits in banks. According to Singapore's definition as seen http://www.mas.gov.sg/data_room/msb/Money_Supply_Compilation_and_Revisions.html M2 is M1 plus 'quasi money'; 'quasi money' defined as something akin to a treasury bill.

There should be no duplicity in the ownership of a unit of currency which makes the Laura example which discussed 'fractional reserve banking' quite irrelevant if not misleading in this respect.

This is because I think that the primary role of money (currency) supply measurement should be the accountability of the central bank in regard of the adequacy of its reserves to balance any claims against its issued currency should a run on the said currency occur.

In the good old days (before Bretton Woods), every US dollar was backed by a defined measure of gold in the vault of the US central bank but no longer; at present, at least some other valid substitute should be required.

Back to the case of M2 being M1 plus 'quasi money'- this is important as it represents the total liability of the central bank issuing such a currency since it is a measure of the total quantity of currency possibly orphaned should current holders of such currency choose concurrently to dispose of such currency. Whatever the value of the currency (or T-bill) in discussion is would then be determined by the amount of foreign currency or other asset that the central bank has in exchange for the said currency now being sold on the international currency exchange market place.

An accurate assessment of the total currency and T-bills of a sovereign in circulation as a ratio of the sovereign assets allocated to validate such liability, pari-passu, is thus integral in any effort to determine an accurate value of a sovereign's unit currency as opposed to that of another. — Preceding unsigned comment added by 220.255.2.70 (talk) 00:19, 7 May 2012 (UTC)

evolution of money supply in africa. case study: cameroon[edit]

what is money supply and the evolutin of money supply — Preceding unsigned comment added by 195.24.220.16 (talk) 20:54, 12 November 2013 (UTC)

Example - Step 10 vs. Step 12 inconsistency[edit]

In the "Laura" example, we read "M0 = 0", at Step 10.

(Mandy's bank now lends the money to someone else who deposits it on a checking account on yet another bank, who again stores 10% as reserve and has 90% available for loans. This process repeats itself at the next bank and at the next bank and so on, until the money in the reserves backs up an M1 money supply of $9000, which is 10 times the M0 money. (MB = $900, M0 = 0, M1 = $9000, M2 = $9000)

A few lines down, at Step 12, we read: "US M0 still has the $900"

But nothing has occurred in between to increase M0 by $900. — Preceding unsigned comment added by Euforbio (talk • contribs) 16:09, 22 December 2013 (UTC)

Discrepancy in description of M0 in the US[edit]

In the 1st table, the only check mark in the M0 column corresponds to the 1st row:

"Notes and coins in circulation (outside Federal Reserve Banks and the vaults of depository institutions) (currency)"

Directly underneath the table you note:

"M0: In some countries, such as the United Kingdom, M0 includes bank reserves, so M0 is referred to as the monetary base, or narrow money."

Which implies that perhaps in the US (which is what the preceding table was about) M0 does NOT include "bank reserves."

And then later in the this section:

http://en.wikipedia.org/wiki/Money_supply#United_States

You write about MO the following:

"M0: The total of all physical currency including coinage. M0 = Federal Reserve Notes + US Notes + Coins. It is not relevant whether the currency is held inside or outside of the private banking system as reserves."

So here it's clear that being inside or outside the private banking system as reserves is "not relevant" to its status as M0, but in the table you clearly state that it's ONLY the currency OUTSIDE depository institutions. This seems to be a direct contradiction. — Preceding unsigned comment added by 68.6.85.103 (talk) 14:40, 10 April 2014 (UTC)

Vault Cash[edit]

Authors here might want to look at some of the information that Mark A. Sadowski has dug up concerning vault cash here. I'm not sure you've got everything straight in this article concerning the US:

http://www.themoneyillusion.com/?p=26531&cpage=2#comment-333251 — Preceding unsigned comment added by 206.190.77.154 (talk) 22:31, 21 April 2014 (UTC)

Here is the definition of "vault cash," in Regulation D of the Federal Reserve System, at 12 C.F.R. section 204.2(k):

- (k)(1) Vault cash means United States currency and coin owned and booked as an asset by a depository institution that may, at any time, be used to satisfy claims of that depository institution's depositors and that meets the requirements of paragraph (k)(2)(i) or (k)(2)(ii) of this section.

- (2) Vault cash must be either:

- (i) Held at a physical location of the depository institution (including the depository institution's proprietary ATMs) from which the institution's depositors may make cash withdrawals; or

- (ii) Held at an alternate physical location if—

- (A) The depository institution claiming the currency and coin as vault cash at all times retains full rights of ownership in and to the currency and coin held at the alternate physical location;

- (B) The depository institution claiming the currency and coin as vault cash at all times books the currency and coin held at the alternate physical location as an asset of the depository institution;

- (C) No other depository institution claims the currency and coin held at the alternate physical location as vault cash in satisfaction of that other depository institution's reserve requirements;